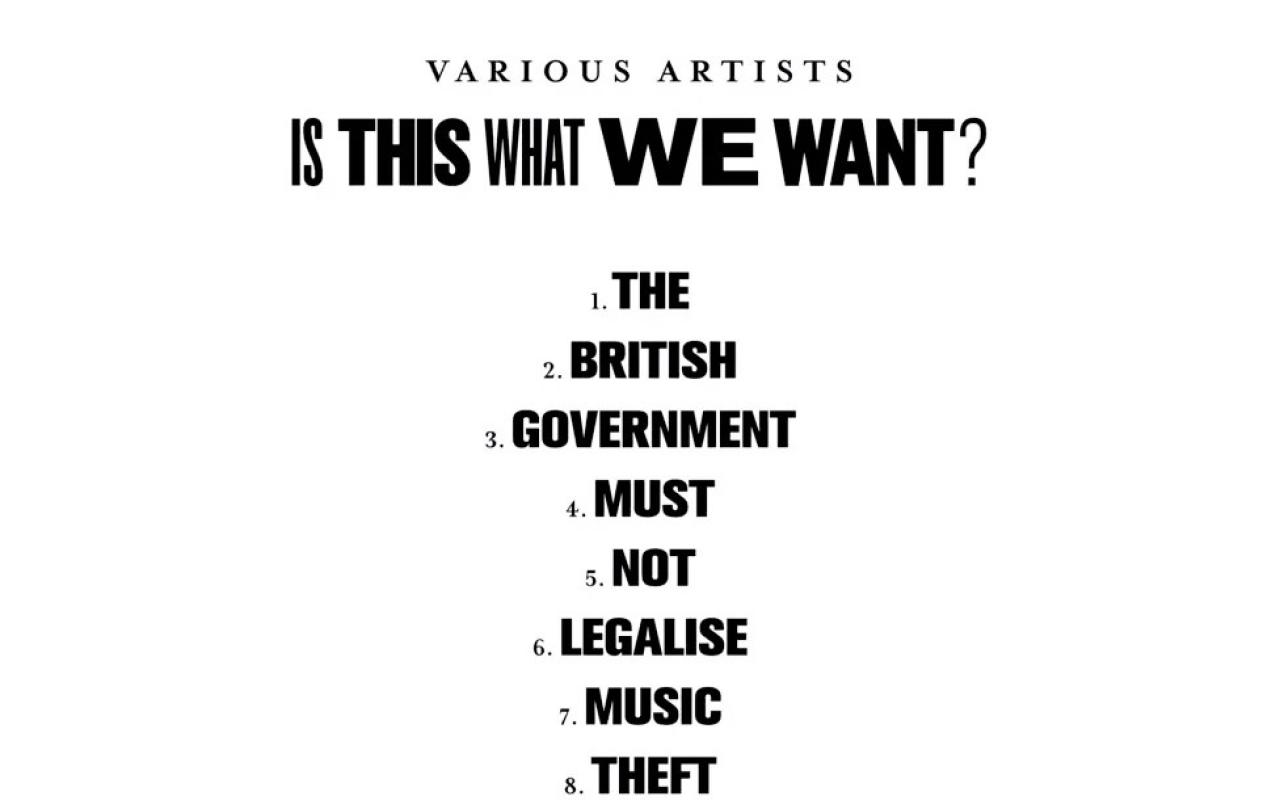

Is the battle between AI and creativity over before it began? A collective of 1,000 musicians have released a silent album to protest new government copyright laws that would make it easier for companies to train AI models without paying artists. The album, titled “Is This What We Want?,” has a tracklist that reads “The British Government Must Not Legalise Music Theft To Benefit AI Companies.”

But this isn’t the first time that new technology has threatened the livelihood of musicians, nor the first time musicians have fought back. And the lesson to be learned from the past is that the real enemy of creativity isn’t technology- it’s greed.

Musicians on strike

The invention of the record player forever changed the music industry. It’s difficult to imagine a time when you could only hear music if someone was playing a live instrument. As music records grew rapidly in popularity, payments to the musicians behind the records lagged behind.

Up until the 1940s, record companies paid studio musicians only for the time in the studio. Playing records on live radio was cheaper than hiring big bands (which had previously been the norm) because the musicians wouldn’t see any revenue from their repeated use. But in August 1942, fed up at the lack of royalties paid from music records, the American Federation of Musicians went on strike.

The silence lasted nearly 2 years. During the strike, musicians were allowed to play for live radio but banned from playing on records.

At first, record companies relied on releasing music they had already recorded. But when it became clear that the strike would last longer than expected, they began to rely on acapella voices in place of big bands for new releases. The strike concluded in 1944 as record players conceded to the American Federation of Musicians and set up a system of paying royalties to musicians. The battle was over.

The technology creativity face-off

Technology has often seemed to be at odds with human creativity despite emerging from it. Human creativity invented the record player, but the record player threatened the human creativity of all those musicians playing live.

In a similar way, artificial intelligence was both invented by creative humans and trained on the work of other creative humans. And yet, its very existence seems to threaten the work of thousands. AI’s threat is felt in every corner of the creative industries- in music, illustration, art, film and photography. And it’s not just a worry for Top 40 singers. Generative AI threatens to replace graphic and web design for small businesses, music in the background of commercials and videos, illustrations on mass produced birthday cards and souvenirs- all areas of creative work where artists receive a modest income and don’t become household names.

Companies use technology as a mirage to hide the real threat behind its computer generated glow- the greed of the human heart.

he Christian faith offers a few truths that make sense of this tension between AI and creativity. The first is human creativity is not mere ornamentation- it is at the very heart of what it means to be made in God’s image. At the very beginning of the Bible, God is Creator. Unlike God, humans cannot make something from nothing. But we can produce wonders that inspire, that reflect the goodness, truth and beauty of the world God created for us. Every string plucked, stitch sewn, brushstroke painted, is a sign that humans were made for more than utility. We were made for transcendence.

The Christian faith also teaches that human selfishness gets in the way of the transcendental vision God has for us.

The invention of the record player created problems for musicians, but it was the unwillingness of companies to pay musicians fairly for their work that posed the real threat. Companies use technology as a mirage to hide the real threat behind its computer generated glow- the greed of the human heart.

As AI continues to be adopted, executives join the chorus speaking about the “threat of AI” and the need to prioritise human creativity. Yet the decisions of the same executives value human creativity in financial terms by the compensation (or lack thereof) that real artists receive.

Companies treat new technologies as inevitable– they might even tell employees that those who can’t learn to use new technology will be left behind. But the reality is that companies shape the direction of technological advancement. There is no “neutral” or “inevitable” direction to technology. Technology can solve human problems- but first humans decide what problems need solving. AI may help us solve problems that benefit all of us- like the work being done to synthesise proteins that can have great impacts in medicine and science.

But there is no reason companies must use generative AI for creative work. People may point to money and time saved, shareholder value created. And this is where the real contradiction lies. For creativity is not a problem that needs to be solved, but a gift for us to partake in.

Is This What We Want?

The album by “1000 UK Artists” contains the sound of empty music studios- a future the group fears if musicians are replaced with AI who were trained on their talent. Session musicians, cover artists, violinists who busk in the streets or play in weddings, all are in danger from AI being trained on their hard work for free.

Knowing that technology is never neutral, the album’s title “Is This What We Want?” poses a good question. What kind of world do we want to live in? What should our technology be building towards?

For me, I want a world that encourages real human creativity– the kind given to us by God, the original creative. I want a world where technology isn’t a way for the rich to become richer but for our communities to become better places for human connection. Technology should give us more time to create art, not less. The battle between creativity and AI is in the hands of lawmakers for now. But the battle to end human greed? That’s eternal.