There’s a man with a black rainhat and jacket on the stage swearing at over 50,000 teenagers. It’s Liam Gallagher, the lead singer of Oasis, that iconic 90s rock band. He’s singing his way through the entire Definitely Maybe album to mark the 30-year anniversary of its release. Somehow, these 50,000 teenagers know all the words, as they sing along on a warm summer evening for their rite of passage that is the Reading Festival.

I feel strangely alone in the crowd. I remember where I was when the album was first released - nobody around me was even born then. On the stage, Liam too is strangely alone. For 15 years he’s been estranged from his brother Noel – the song-writing genius behind all of Oasis’ greatest hits. He’s in a reflective mood as he sings ‘Live Forever’:

“Maybe I will never be, all the things that Ii want to be, now is not the time to cry, now’s the time to find out why”

(Live Forever)

This lyric has aged well. Back when Liam was 21 years old, about to be biggest band in the world, about to see their album become the fastest selling debut album of all time, he wasn’t seriously considering the question.

Back then, fame didn’t seem to suit him. He famously ditched a huge US tour with the band, when he was about to board the plane from Heathrow. He stubbornly refused to go on stage for the MTV unplugged concert at the Royal Festival Hall despite a packed-out audience and a full orchestra on the stage. Maybe it was youth. Maybe it was anxiety. Maybe it was some illegal substance.

Even now, at Reading, with rumours rife of a reunion tour, Liam seems a little vulnerable. He delivers a brilliant vocal performance to a huge crowd, but his hat covers most of his face for the entire concert. He mentions that he had thought the young people getting their GCSEs might have let their academic excellence go to their heads, but they turned out to be “alright” after all. And then, with more swearing, more swaggering guitar chords and more defiant sneering vocals, there comes more vulnerability:

Their song brought the country together in a pledge of hope. While terrible things are going on around us in our world, we need all the togetherness and hope we can get.

“All this confusion, nothings the same to me, I can’t tell you the way I feel, because the way I feel is oh so new to me”

(Columbia)

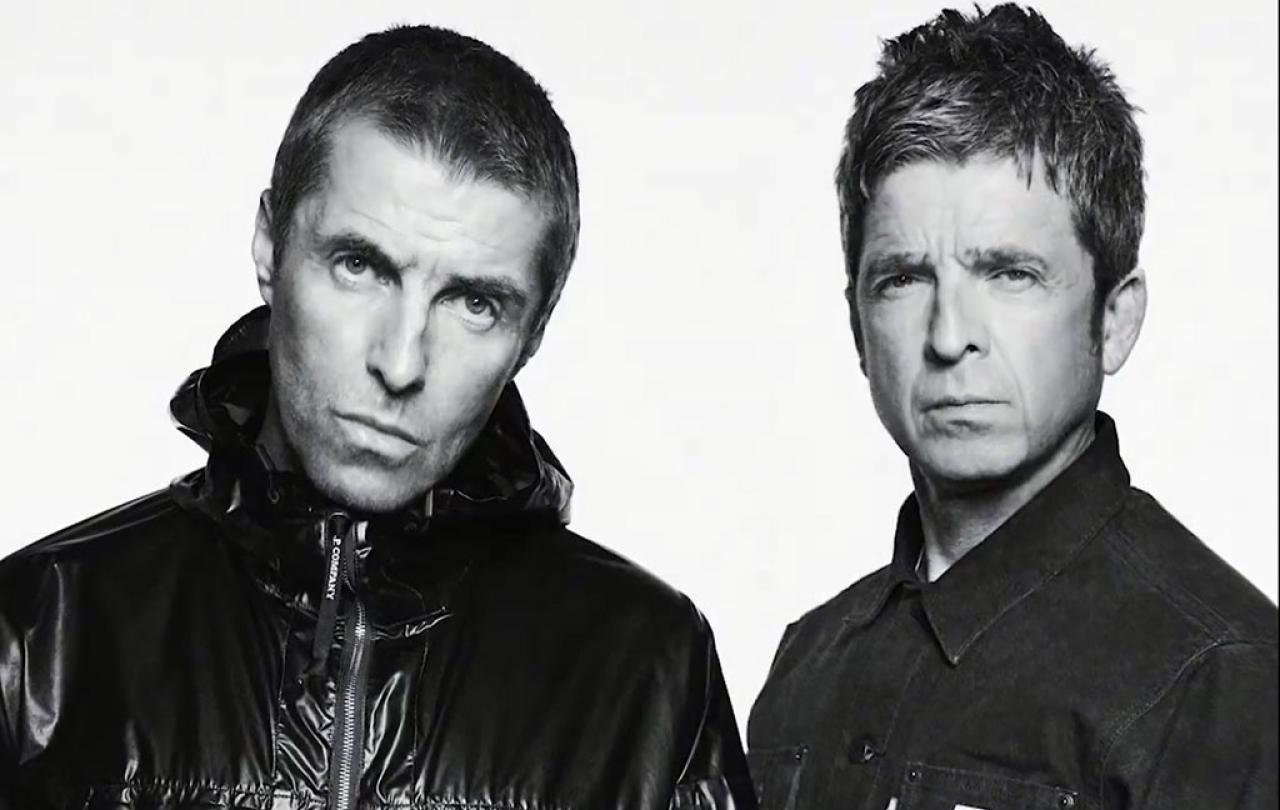

Liam dedicates “Half a World Away” to his brother Noel, and then the promise of something more… “27/08/2024 8am” is revealed on the huge screen. Is there going to be more to the Oasis story? Could the feuding brothers have buried the hatchet? Have they listened to their own lyric – don’t look back in anger – and decided to drop the bitterness and animosity and find a new way forward?

I wonder how the reconciliation happened. I like to imagine it was like Joseph, Prince of Egypt and wearer of coat-of-many-colours, finding himself face-to-face with the brother who tried to murder him all those years earlier, and privately breaking down in tears before declaring “God meant it for good”.

I like to imagine it was like Joseph’s father Jacob, Patriarch of Israel and hot-headed runaway, returning to his twin brother Esau after two decades of separation, praying he would be received favourably, and overwhelmed when his prayer was answered.

‘Some might say’, excuse the pun, that the timing of this impossible reconciliation is less to do with making peace and more to do with making money. The Gallagher brothers have both been through costly divorces. Perhaps they have seen the appetite for megatours as demonstrated by Taylor Swift’s Era’s extravaganza.

A few days later there is controversy brewing around dynamic pricing which is adding to the rumours of extortionate profiteering. Presale tickets initially range from £73 to £205, with standing tickets priced around £150. Then resale prices skyrocket, with some tickets listed for as much as £6,000—approximately 40 times the original price. It remains uncertain how much of these profits Oasis directly receives.

And then there is the timing. Next year the ownership of the Oasis back-catalogue reverts back to Noel. Only a few months ago Queen sold the rights to their back-catalogue to Sony Music in a record-breaking $1.27 billion, surpassing previous deals such as Bruce Springsteen's sale for $500 million. A sell-out tour will go a long way to upping the value of the Oasis catalogue.

Whatever the motivations, whoever is profiting, and however genuine the reconciliation, the reforming of Oasis, in my eyes, is a great moment for our country. I’ll never forget the woman who spontaneously sang “Don’t Look Back in Anger” after the minute’s silence to remember the 22 Ariana Grande fans killed at the Manchester Arena terrorist attack in 2017. While Noel and Liam were still feuding, their song brought the country together in a pledge of hope. While terrible things are going on around us in our world, we need all the togetherness and hope we can get.